The Reserve Bank of Australia has announced a further reduction to the official cash rate by 0.25% as of 12th August. This decision sees the official rate drop to its lowest level in years and is expected to flow through to mortgage rates across the country, with some of the major banks and lenders announcing the passing of the rate cut on in full within hours of the RBA’s announcement.

While a lower interest rate on its own will reduce repayments slightly, this environment also creates an opportunity to restructure your home loan in a way that delivers a much more substantial and lasting impact on your household cash flow.

Using a Lump Sum Deposit to Your Advantage

If you have access to a significant amount of cash — from savings, the sale of an asset, a bonus, or inheritance — you might think about putting it into your mortgage. Many borrowers use an offset account or redraw facility, but there’s another strategy worth considering:

- Deposit the Lump Sum directly into the loan, reducing the principal immediately.

- Capitalise the New Loan Amount by asking your lender to recalculate the loan based on the reduced balance, removing the redraw access.

- Reforecast the Loan Term & Repayments using the lower principal and lower interest rate.

The result is a permanent reduction in your monthly repayments — which frees up cash flow that can be directed toward other financial goals.

Why This Matters for Cash Flow

- Immediate Repayment Reduction: A lower principal and lower rate combine to shrink monthly commitments.

- Budget Simplicity: No redraw means less temptation to dip back into the loan.

- More Financial Flexibility: The extra monthly funds can go to savings, superannuation, or investments.

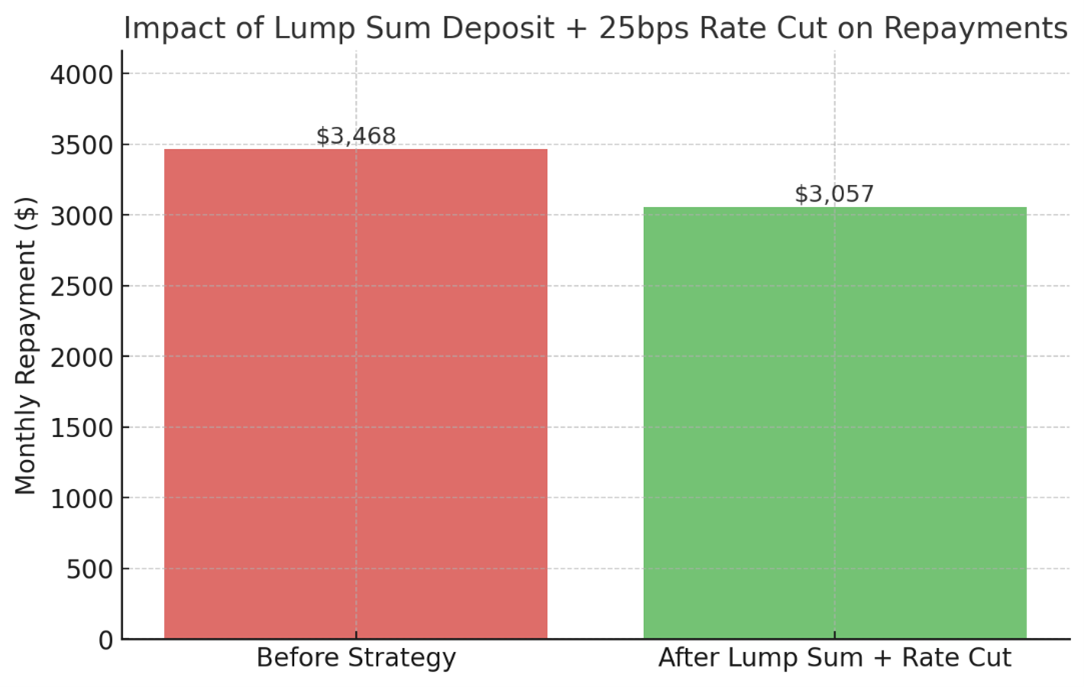

A Quick Example

Let’s take a $500,000 home loan with 20 years remaining at a rate of 5.6%.

- You make a $50,000 lump sum deposit.

- The RBA cuts rates by 25 basis points, bringing your rate down to 5.35%.

- Your lender removes redraw and recalculates repayments on the new balance of $450,000 over the same term.

Here’s the difference:

In this example, monthly repayments drop by hundreds of dollars — creating a meaningful and lasting cash flow improvement.

Final Thoughts

With rates easing, don’t just accept the minimal savings from the bank’s automatic rate adjustment. By combining a lump sum deposit with a re-forecasted loan term, you can lock in a permanent repayment reduction and give yourself breathing room in the household budget.

Before making changes, speak with your lender or financial adviser to ensure this strategy suits your overall financial plan.

Written by

Aaron McInnes

Financial Planner | Mortgage Broker

Grad.DipFS(FP), DipFS(FMBM), SMSF Adviser