In investing, it’s tempting to focus on the upside. Higher returns, stronger rallies, and outperforming the market during good times are what grab headlines and fuel dinner-party conversations. But over long periods, the real determinant of investor success is not how high a portfolio climbs in the best moments, it’s how well it protects capital when markets fall.

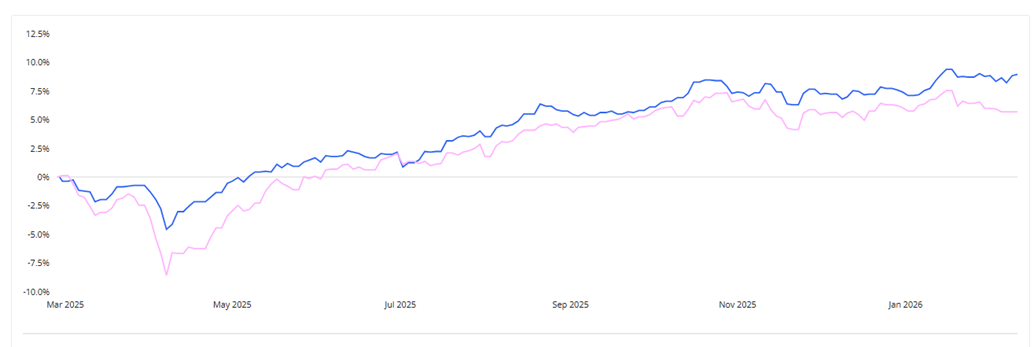

The chart below comparing the MIC Retire 70 Managed Portfolio (blue) with a comparable index fund (pink) makes this point clear. Both portfolios participate in market growth over time. However, the difference emerges most sharply during periods of stress, particularly around “Liberation Day” in April 2025, when Donald Trump stood on The White House lawn and announced sweeping tariffs on other countries. Markets reacted swiftly, and volatility spiked.

While the index fund experienced a sharp drawdown, the MIC Retire 70 portfolio fell less and recovered faster. That difference may look modest on a chart, but its impact compounds meaningfully over time.

Losses Hurt More Than Gains Help

One of the most overlooked realities in investing is that losses and gains are not symmetrical. A 10% loss requires an 11% gain just to get back to even. A 20% loss needs 25%. A 50% loss? A 100% gain.

This maths alone explains why downside control matters. Every extra percentage point lost during a market downturn creates a higher hurdle for recovery. Portfolios that fall less don’t need heroic returns to regain lost ground, they simply keep moving forward while others are still catching up.

Behaviour Matters as Much as Returns

Downside protection isn’t just about numbers; it’s about investor behaviour. Large drawdowns increase the likelihood of poor decisions: panic selling, abandoning a strategy, or sitting in cash while markets recover.

During the tariff-driven sell-off in early 2025, investors in the index fund saw deeper and faster losses. For many, that kind of drawdown triggers fear and second-guessing. In contrast, portfolios that experience smaller declines are easier to stick with. Staying invested through volatility is one of the most powerful drivers of long-term returns and it’s far easier when losses are controlled.

Recovery Time Is Opportunity Cost

The chart also highlights another crucial concept: time spent recovering is time not spent growing.

After Liberation Day, the MIC Retire 70 portfolio regained its previous high earlier than the index fund. That earlier recovery allowed it to participate fully in subsequent market gains, while the index fund was still climbing out of its hole. Even if both portfolios eventually reach similar levels, the smoother path creates a higher effective return for the investor.

In retirement-focused portfolios, this matters even more. Investors drawing income during downturns are forced to sell assets at depressed prices, permanently impairing capital. Minimising drawdowns reduces this risk significantly.

Upside Still Matters — Just Not at Any Cost

None of this suggests that upside is irrelevant. A portfolio that never grows is not a solution. But maximising upside without regard for risk is a fragile strategy. Markets are unpredictable, geopolitics can shift overnight, and events like tariff announcements remind us how quickly sentiment can change.

A well-constructed portfolio aims to capture a meaningful portion of market upside while actively managing risk on the downside. Over full market cycles, this approach often delivers more consistent outcomes, lower stress, and better investor experiences.

The Quiet Advantage

Minimising the downside rarely makes headlines. It doesn’t feel exciting in booming markets. But as the comparison between the MIC Retire 70 Managed Portfolio and the index fund shows, it is during periods of uncertainty, like Liberation Day, that risk management quietly does its most important work.

In the end, successful investing isn’t about winning every rally. It’s about staying in the game long enough, and with enough capital intact, to let compounding do its job.

Written by

Michael Simmons

Senior Financial Adviser

Milestone Financial, Canberra